Bitcoin price sits around $115,000 as the Federal Reserve meets this week. Policy risk concentrates around Wednesday’s Oct. 29 decision at 2 p.m. ET, followed by Chair Jerome Powell’s press conference at 2:30 p.m. ET. Markets price a 25 basis point cut for this meeting with further easing odds into year end, according to the CME FedWatch methodology that maps fed funds futures to meeting-by-meeting probabilities. The setup ties directly to Bitcoin’s macro channel, where guidance on the front end transmits to 10-year real yields and the dollar, then into ETF demand and derivatives positioning on the tape. Flows frame the week. U.S. spot Bitcoin ETFs swung from a large outflow on Oct. 16 to a large inflow on Oct. 21, then a modest net gain on Oct. 24. Concentration remains in the leaders, with cumulative nets since launch at IBIT plus $65.3 billion, FBTC plus $12.6 billion, and GBTC minus $24.6 billion, according to Farside. Breadth outside the top two issuers has been inconsistent, which makes the policy tone a near term driver of allocation follow-through after the decision window. Date Total US spot BTC ETFs net flow (USD m) Notes Oct. 16 -531 Outflow burst Oct. 21 +477 Snapback day Oct. 24 +33 IBIT +58 Positioning is heavy into the event. Options open interest sits near record territory on Deribit, which raises gap risk around headlines and the press conference cadence. Perpetuals funding across major venues has run modestly positive with high aggregate futures open interest, according to CoinGlass. That mix can be a catalyst for two-way wicks if the path deviates from pricing. The Oct. 17 risk-off session that saw roughly $147 million in BTC liquidations tracked by CoinGlass illustrates the wipeout potential when positioning is crowded. Macro context has shifted over the past two months. The policy path has repriced toward cuts into the Oct. 28 to 29 meeting, per CME FedWatch, while parts of the U.S. data flow have been impaired by shutdown disruptions that complicate visibility. Real yields eased from summer highs, with the 10-year TIPS proxy around 1.7 percent late last week, and the dollar stabilized, with a pop against the yen into Fed week. Those variables matter for digital asset risk appetite, since BTC has shown episodes of strong inverse correlation with U.S. real yields and tends to lag when the dollar firms, although the relationship is state-dependent and can break down. Mechanically, a 25 bp cut combined with a cautious tone would anchor front-end expectations, which would tend to keep 10-year real yields flat to slightly lower and the dollar steady to softer. Under that path, ETF nets could skew mixed to modestly positive with a chance of broader participation beyond the top two if Powell avoids hawkish twists, while the spot tape trades range-bound with buy-the-dip interest around presser volatility. A more dovish 25 bp paired with an easing bias or softer labor acknowledgments would be expected to shave real

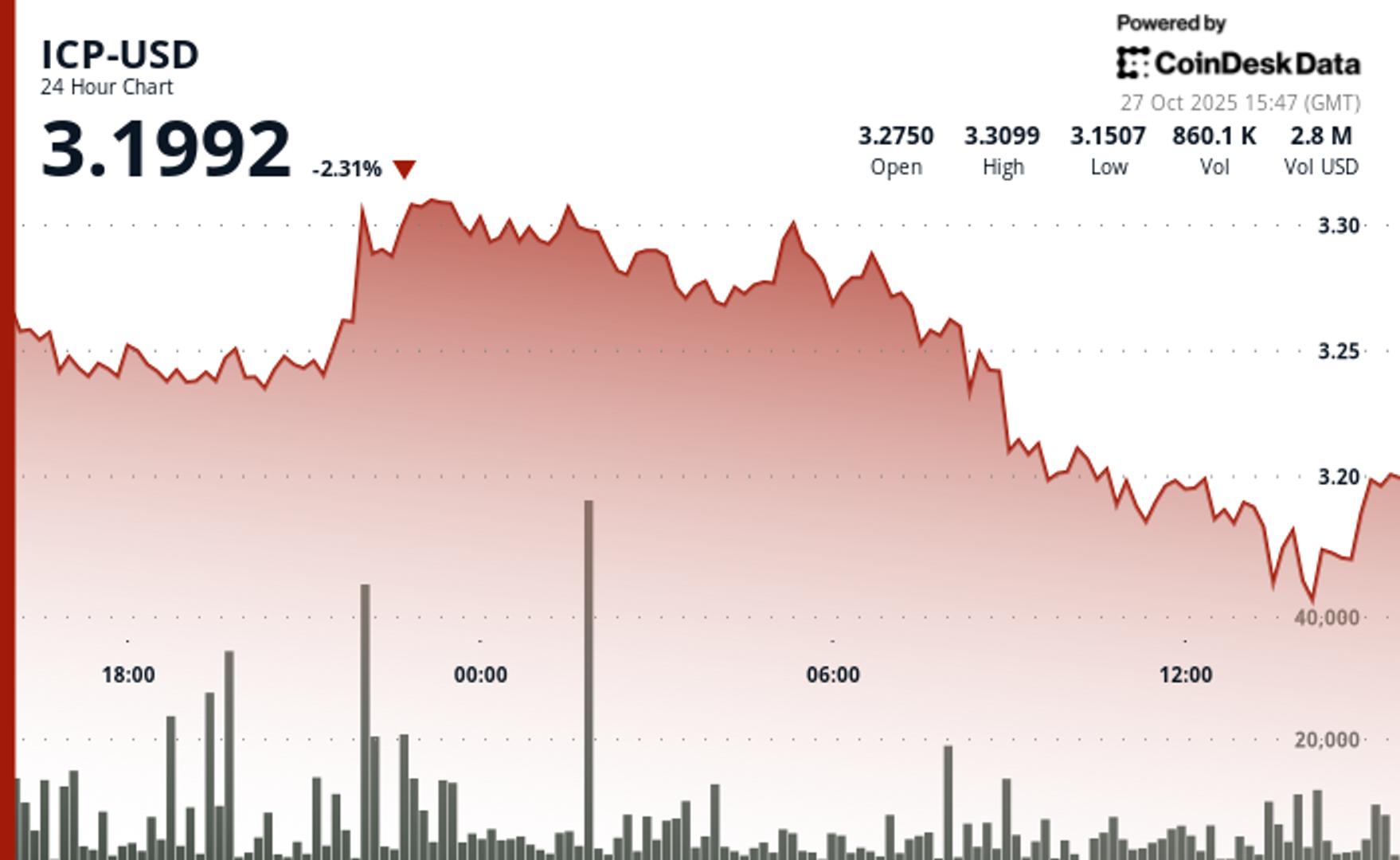

Crypto’s week ahead: Everything you need to know to close out October